Student Loans Resource & Financial Education

Source: sonicmusic.net

Welcome to our Student Loans resource center — a place dedicated to helping students, graduates, and families better understand the world of education financing. Here we discuss federal and private student loans, repayment strategies, interest rates, forgiveness programs, and practical ways to manage education debt with greater confidence.

You’ll find clear explanations of how student loans work, step-by-step guidance on applying for loans, comparisons of repayment plans, and helpful tools such as loan calculators and financial planning tips. We also explore topics like loan forgiveness programs, deferment and forbearance options, refinancing, and ways to reduce long-term borrowing costs.

Read more

Top Stories

Read more

Read more

Read more

Read more

Trending

Read more

Read more

Latest articles

Most read

Read more

Read more

In depth

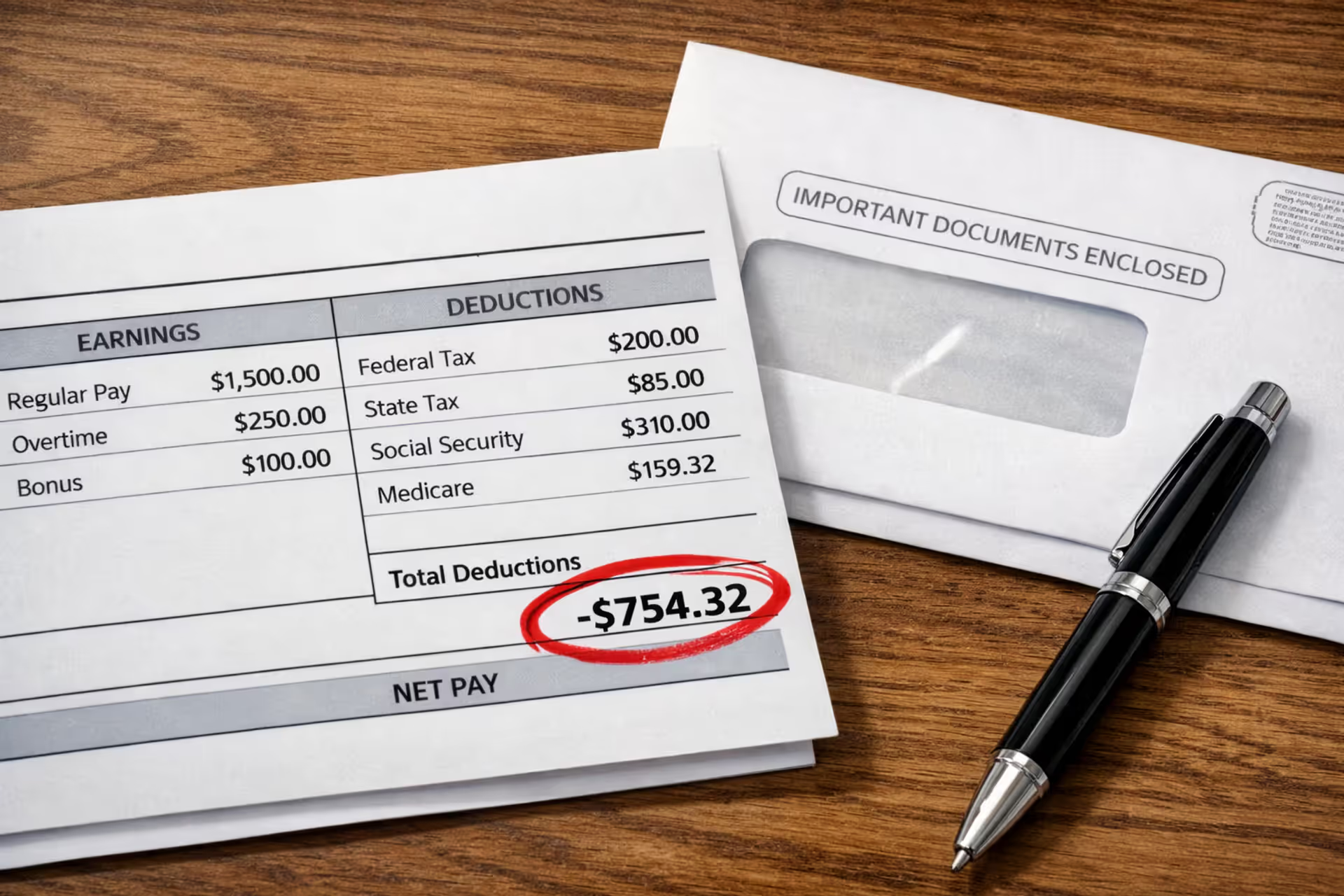

If you've ever stared at a student loan bill and wondered whether you could just swipe a credit card to make it go away, here's the short answer: your loan servicer probably won't let you. The Department of Education banned federal loan servicers from taking credit cards years ago, and private lenders like Sallie Mae or Discover Student Loans won't process card payments either. They'll only pull money straight from your bank account.

But there's a workaround. Third-party companies will charge your Visa or Mastercard, then mail or wire the money to your loan servicer—charging you 2-3% for the privilege. Whether that makes any financial sense depends entirely on your situation. For 95% of borrowers, it's throwing money away. For the other 5% chasing credit card bonuses or juggling a cash crunch, it might be worth the hassle.

Let's break down when it works, when it doesn't, and what happens if you get it wrong.

Why Most Student Loan Servicers Don't Accept Credit Cards

Federal loan servicers—MOHELA, Aidvantage, Nelnet, EdFinancial—all operate under Department of Education mandates that explicitly forbid credit card processing. The government's reasoning? They don't want you piling 22% APR credit card debt on top of your 5% student loans. It's a borrower protection measure disguised as a policy restriction.

Transaction fees are the other sticking point. Visa and Mastercard take 2-3% of every swipe. On a $500 monthly payment, that's $10-15 vanishing into processing costs. Federal servic...

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.